In recent years, the temporary and traveling exhibition format has experienced something of a reinvention. What was once largely the domain of museums and specialty producers has become a battleground for immersive art operators and major intellectual property (IP) holders alike. During the pandemic era, immersive exhibitions surged in popularity, and global entertainment brands like Netflix, Disney, Universal Studios entered the field.

At their best, traveling exhibitions represent the purest form of attractions. They thrive on novelty and artificial scarcity. The fact that they are temporary creates urgency. Each new city offers a new audience encountering the concept “for the first time,” or at least for “the first time in a while”, allowing a show to feel like a premiere again and again.

This freshness is part of its appeal. But the same characteristics that create excitement also create fragility.

Raw Economics

The elements that make touring exhibits appealing are precisely their weaknesses: in a temporary or traveling format, every exhibit is effectively a reset. New lease or venue agreements must be negotiated. Transportation and installation costs recur. Marketing must start from scratch. Staff must be hired and trained. Even in the most “plug-and-play” concepts, the exhibition may travel, but the production effort largely begins anew each time.

We can see the difficulty of the economics in the cases of two high profile exhibition companies that went bust.

Premier Exhibitions

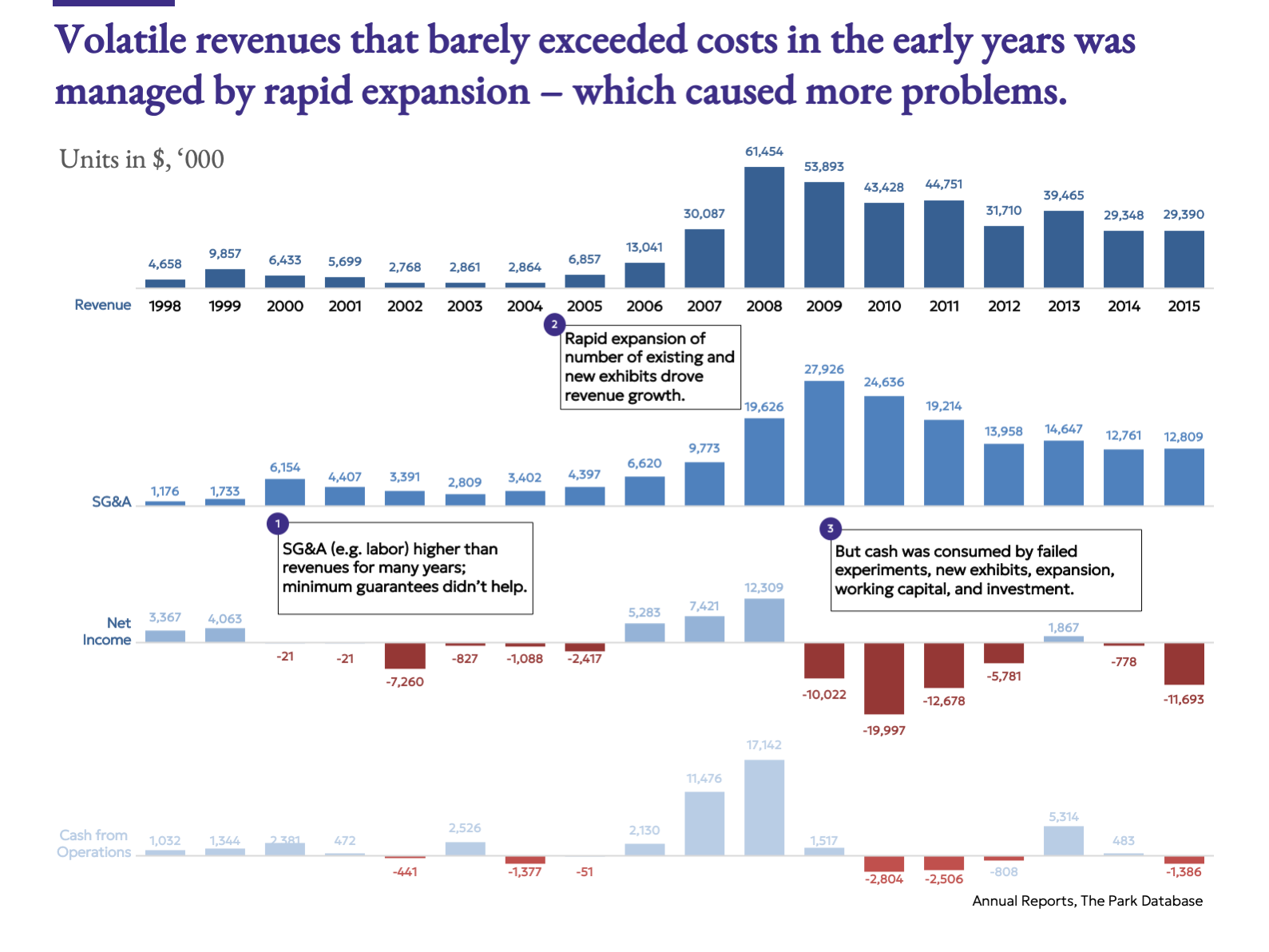

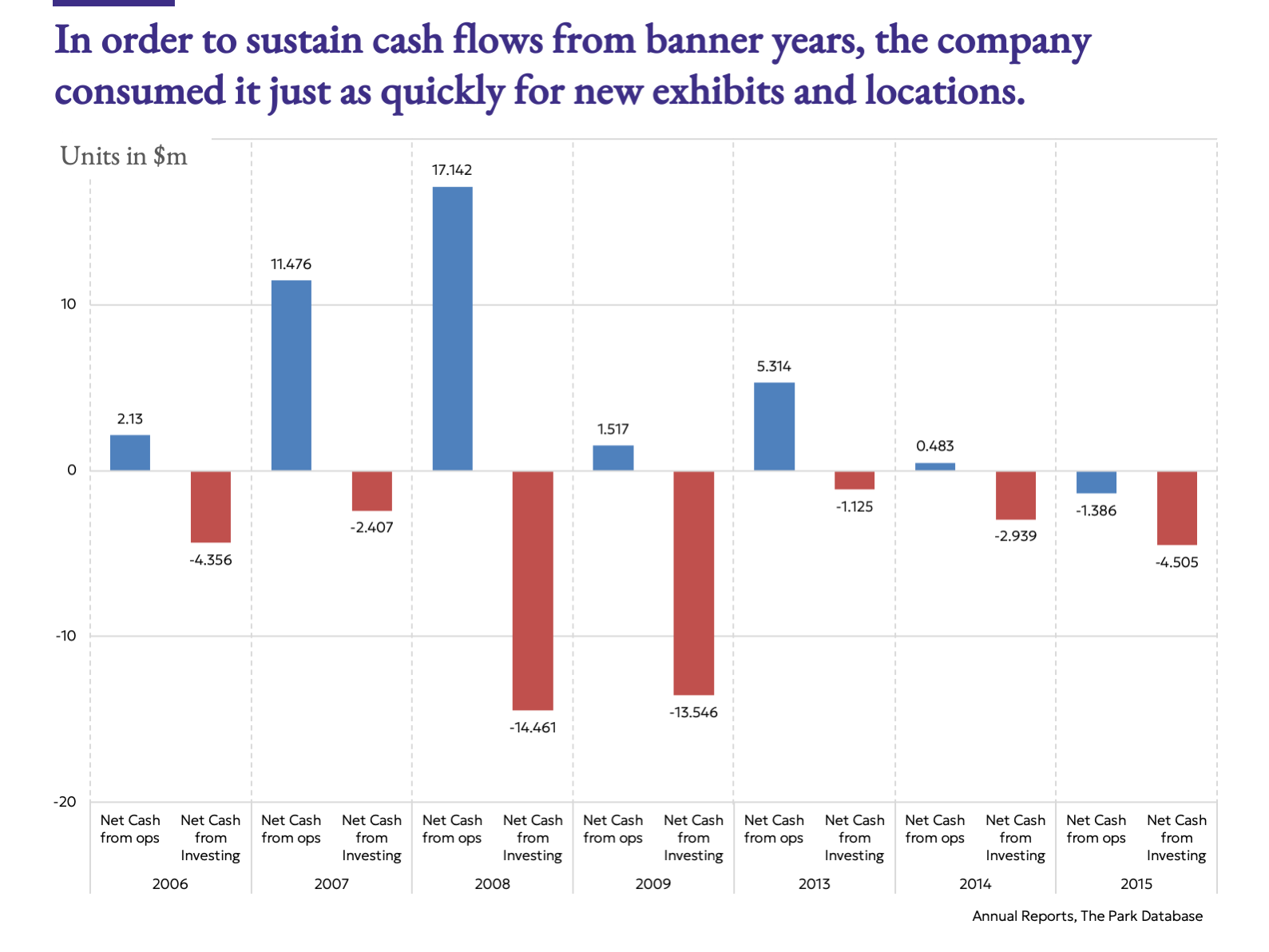

Consider Premier Exhibitions, the excavator and sole exhibitor of Titanic artifacts. On paper, it possessed an enviable asset: exclusive control over one of the most famous archaeological discoveries in modern history. In practice, that control did not translate into stable economics.

Before its bankruptcy in 2016, the company cycled through multiple concepts and operating models, illustrating the inherent difficulty of the touring model:

- In 2011, after a brief experiment in self-operating its Bodies exhibitions, the company exited the self-operated model and laid off staff, and citing operational challenges.

- In 2013, Hurricane Sandy forced the closure of its South Street Seaport location in New York, which had accounted for $4.1 million in revenue. Revenues fell by 25% that year, largely due to the loss of this single site.

- In 2015, the company made a near all-or-nothing bet on a Saturday Night Live exhibition in New York, signing a 51,000 square foot lease, with $38 million in total rent due over 10 years. Concerned about this move and others, the company’s own auditors flagged it as a going concern risk, given Premier’s history of losses and liquidity situation. When attendance failed to meet expectations, the company shut down the SNL Exhibition in 2016, and unable to make the space’s monthly rent, filed for bankruptcy.

Over two decades of operations, the company’s strategic responses to managing the exhibition format often compounded its problems. To reduce volatility, it pursued long-term leases. But when visitation underperformed, those leases became liabilities.

In the 1990s, the company had earlier partnered with SFX Entertainment, which paid minimum guarantees in exchange for exhibition rights. That arrangement stabilized revenues but ceded control and upside. When SFX declined to renew on similar terms, revenues fell nearly 30% in a year and dropped to roughly 27% of their 2002 peak.

Premier’s response to this earlier crisis laid the foundation for its later problems. The company responded by self-operating exhibits and adding more exhibitions in more locations. But scale required capital – production, logistics, marketing – which strained cash flow. What looked like diversification became multiplication of risk. Cash flow generated in banner years went straight out the door to build out exhibitions, pay employees, and long-term leases. And when the various concepts didn’t play out as envisioned, the company’s vulnerabilities were exposed.

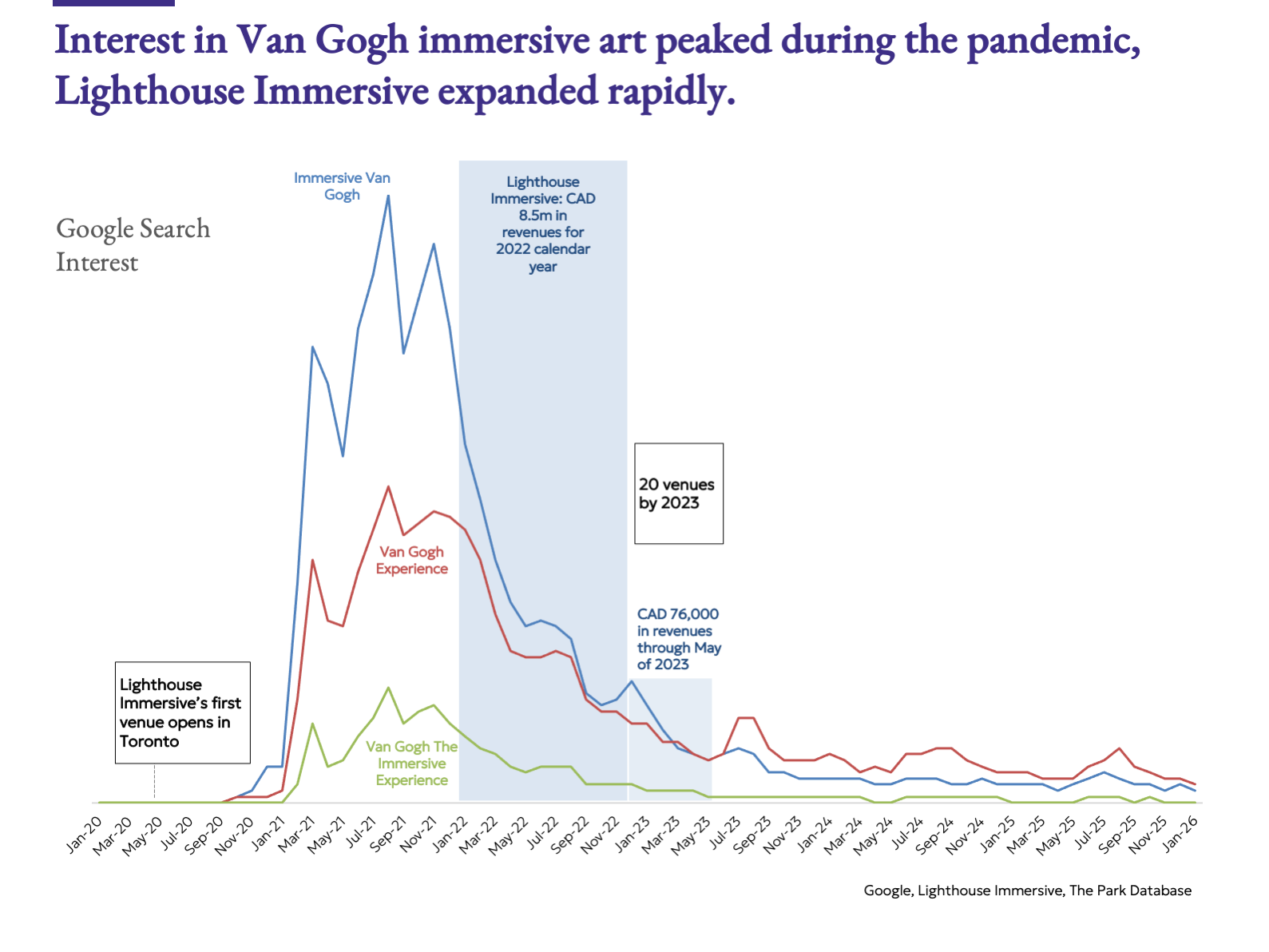

Lighthouse Immersive

In May 2020, in the depths of the pandemic, Lighthouse opened the drive-through Immersive Van Gogh experience in Toronto that met with such explosive demand, it expanded the concept rapidly across North America, signing agreements for 20 venues in a matter of two years.

The company rode a wave of repressed demand, as consumers starved for out-of-home experiences flocked to immersive art installations. But as reopening spread and competing venues proliferated – many undercutting prices – attendance fell sharply.

By the first half of 2023, revenues had shrunk to roughly one-tenth of the comparable 2022 period. Within three years of opening its first location, Lighthouse entered bankruptcy.

Lighthouse’s case illustrates another structural weakness of the exhibit model. Temporary formats invite imitation. With no permanent operator embedded in a market, competitors can fill gaps between tour stops – or launch their own versions entirely.

Because economics are tight, there is also a bias toward concepts that are easily replicated or based on public-domain material, with the result being low defensibility and commoditization.

A Crowded Field

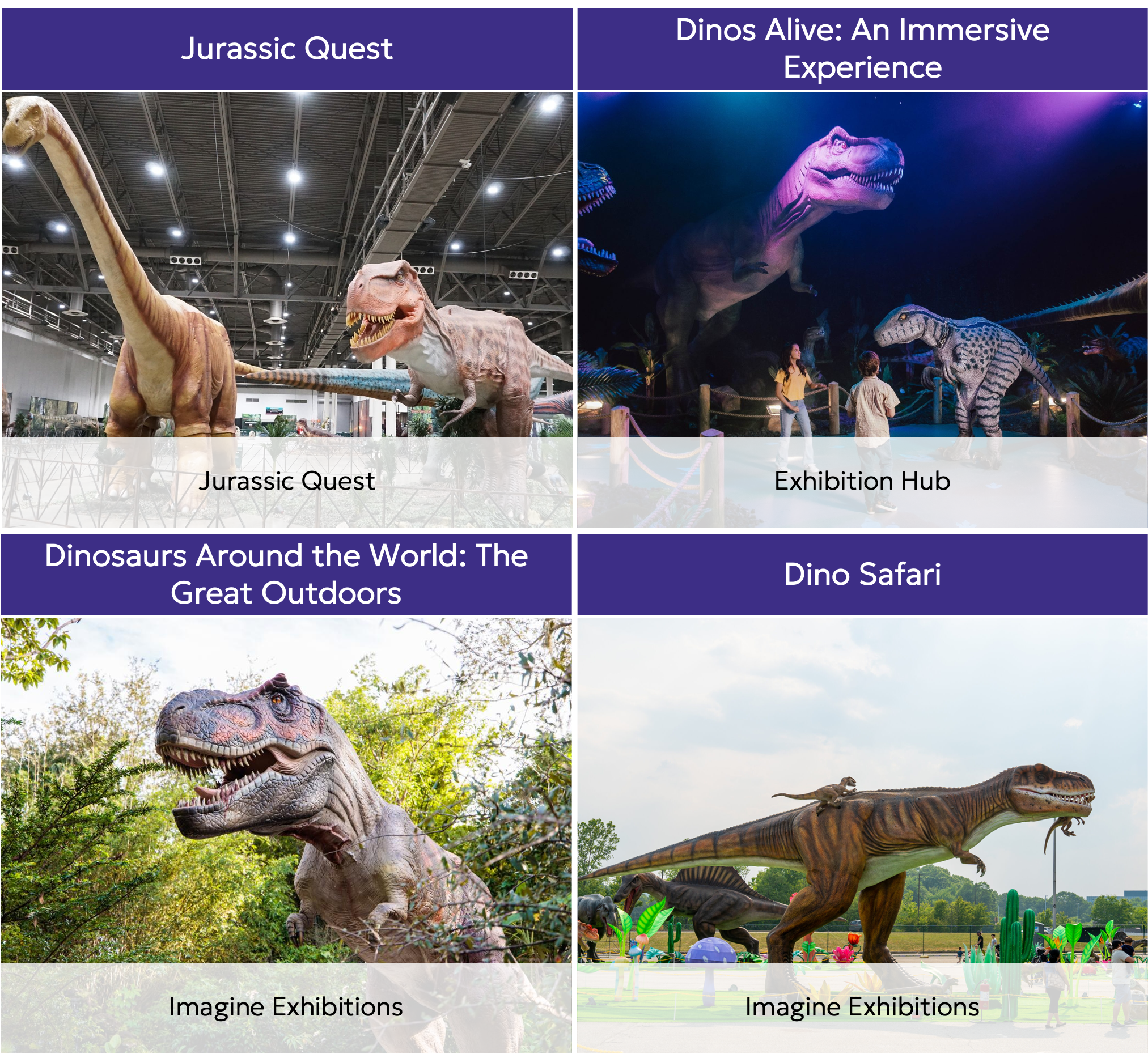

The current touring landscape illustrates the last point. Consider the number of dinosaur-themed exhibits currently on tour:

- Jurassic Quest

- Dinos Alive: An Immersive Experience

- Dino Safari

- Dinosaurs Around the World: The Great Outdoors

- Dinosaur World Live

- Jurassic World Live Tour

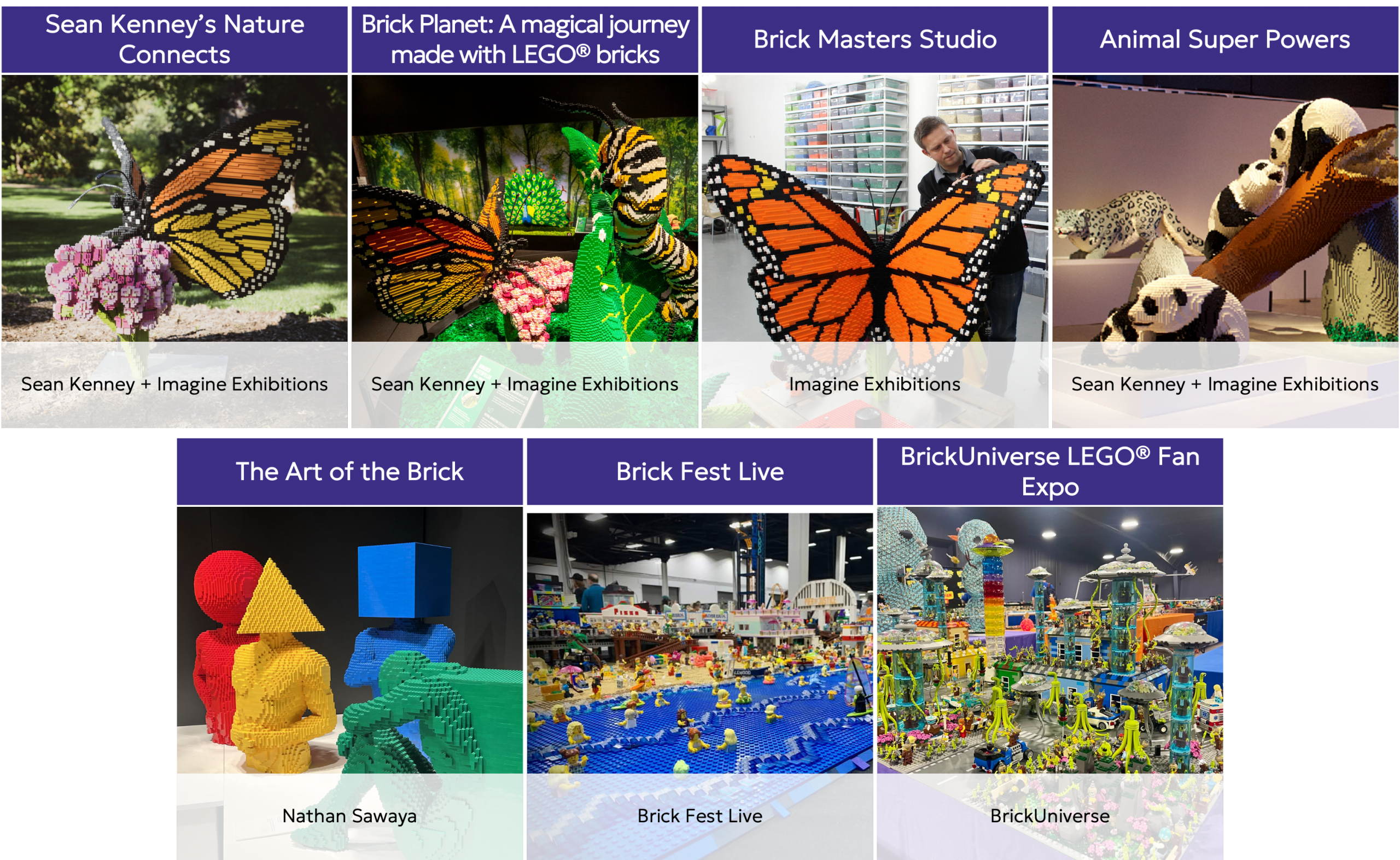

Or LEGO exhibits:

- The Art of the Brick

- BrickUniverse: Immersive Brick Experience Tour

- Brick Fest Live

- BRICKLIVE Brickosaurs (LEGO + dinosaurs, sure to be a fan favorite)

- Brickwrecks

- Sean Kenney’s Nature Connects

- Brick Planet

- Jurassic World by Brickman

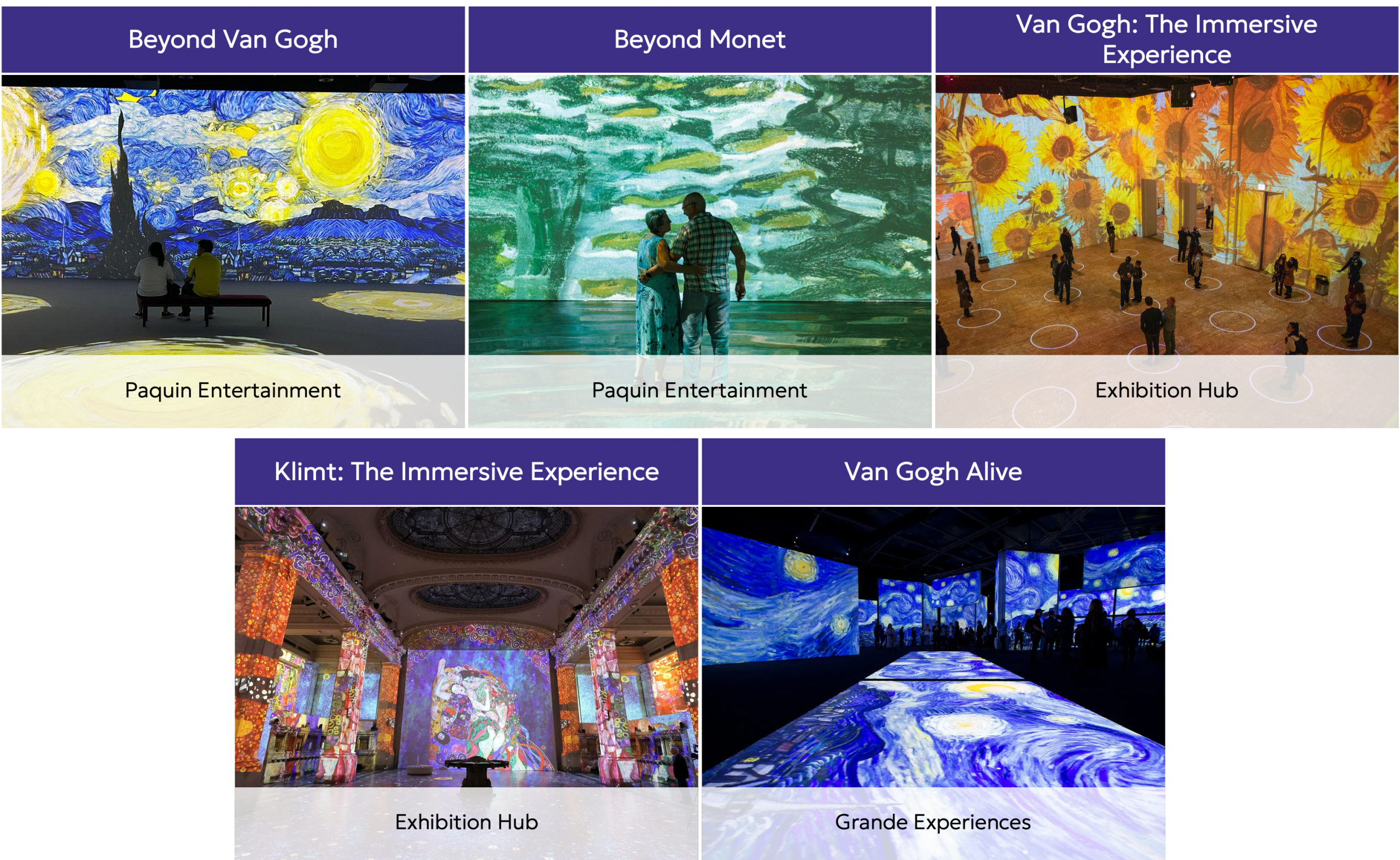

Or art masters:

- Van Gogh: The Immersive Experience

- Beyond Van Gogh: The Immersive Experience

- Beyond Monet: The Immersive Experience

- Monet & Friends Alive

- Van Gogh Alive

- Klimt: The Immersive Experience

The pandemic created a surge of pent-up demand that found expression in immersive experiences once the world reopened. But the very openness of the format—few structural barriers, public-domain material, flexible production—enabled waves of similar shows to enter the market simultaneously.

The Upside

If the economics are so volatile, why participate at all?

Because the upside can resemble theme park-level performance in compressed timeframes.

Certain touring exhibitions have endured for decades. Nathan Sawaya’s Art of the Brick has toured for nearly thirty years, with over 10 million visitors. Body Worlds has done the same, with nearly 60 million in attendance. Harry Potter: The Exhibition has toured globally since shortly after the publication of Harry Potter and the Deathly Hallows.

At their peak, individual shows can generate extraordinary revenue with comparatively modest fixed infrastructure. Other reasons might be strategic in nature: the temporary format also allows risk-sharing between producer and host venue, reducing capital intensity compared to building permanent attractions.

Success Factors

Traveling exhibitions and experiences are structurally fragile, easily replicated, yet capable of extraordinary cultural and financial impact.

And often, the difference seems to not be in the artifact or content itself – but in the narrative, timing, marketing intensity, design, positioning.

The success of the immersive art masters genre is an example. The paintings of artists like Van Gogh and Monet are in the public domain and have been for years. But projection mapping, sound design, and floor-to-ceiling environments reframed their presentation as novel, and a single company – Lighthouse Immersive – sold 5 million tickets for Van Gogh exhibits within two years.

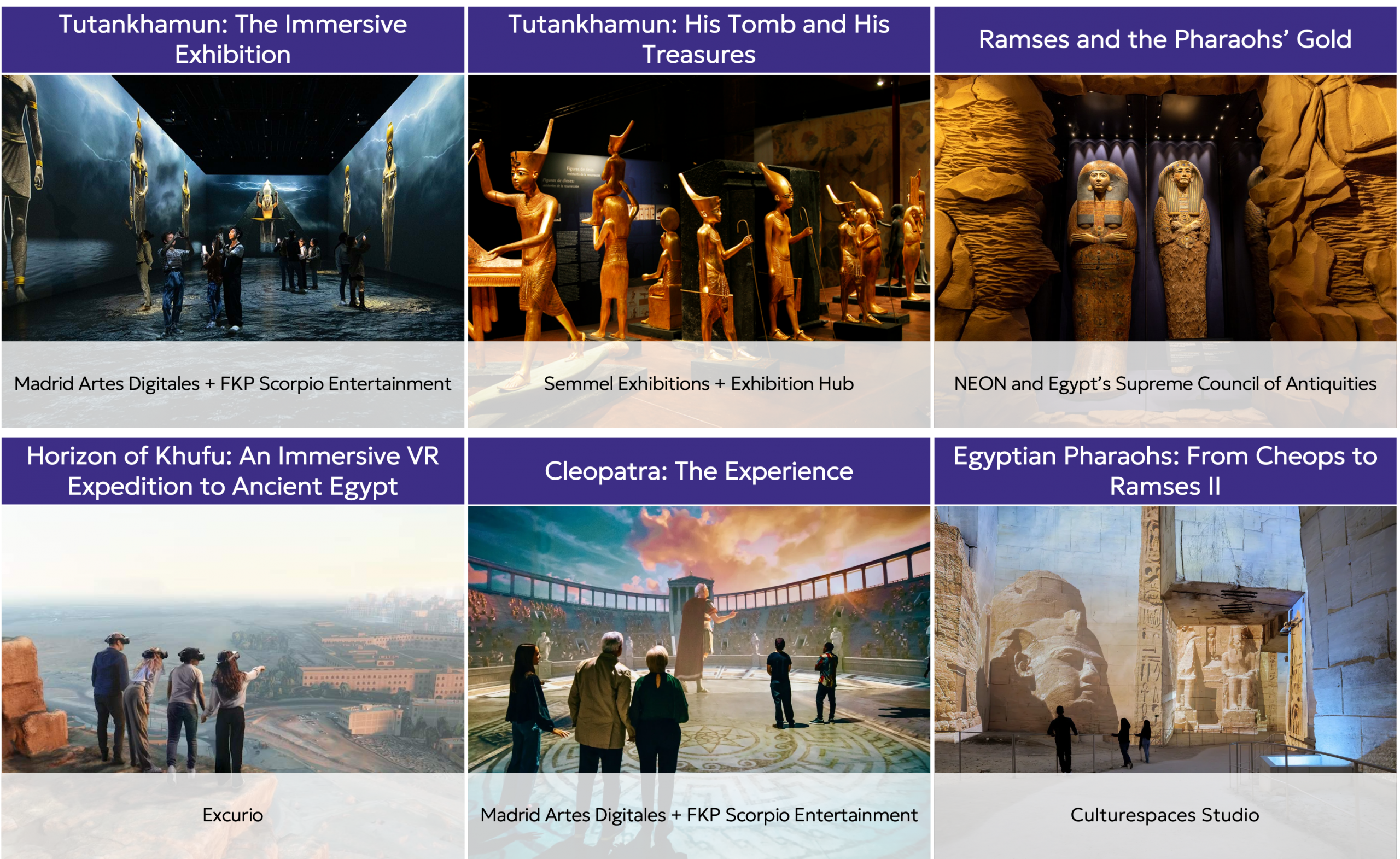

A new format can create a fresh product, even from centuries-old material, and if we go even further back, history provides one of the clearest examples of this point: the Tutankhamun exhibitions in the United States.

Tutankhamun Tours

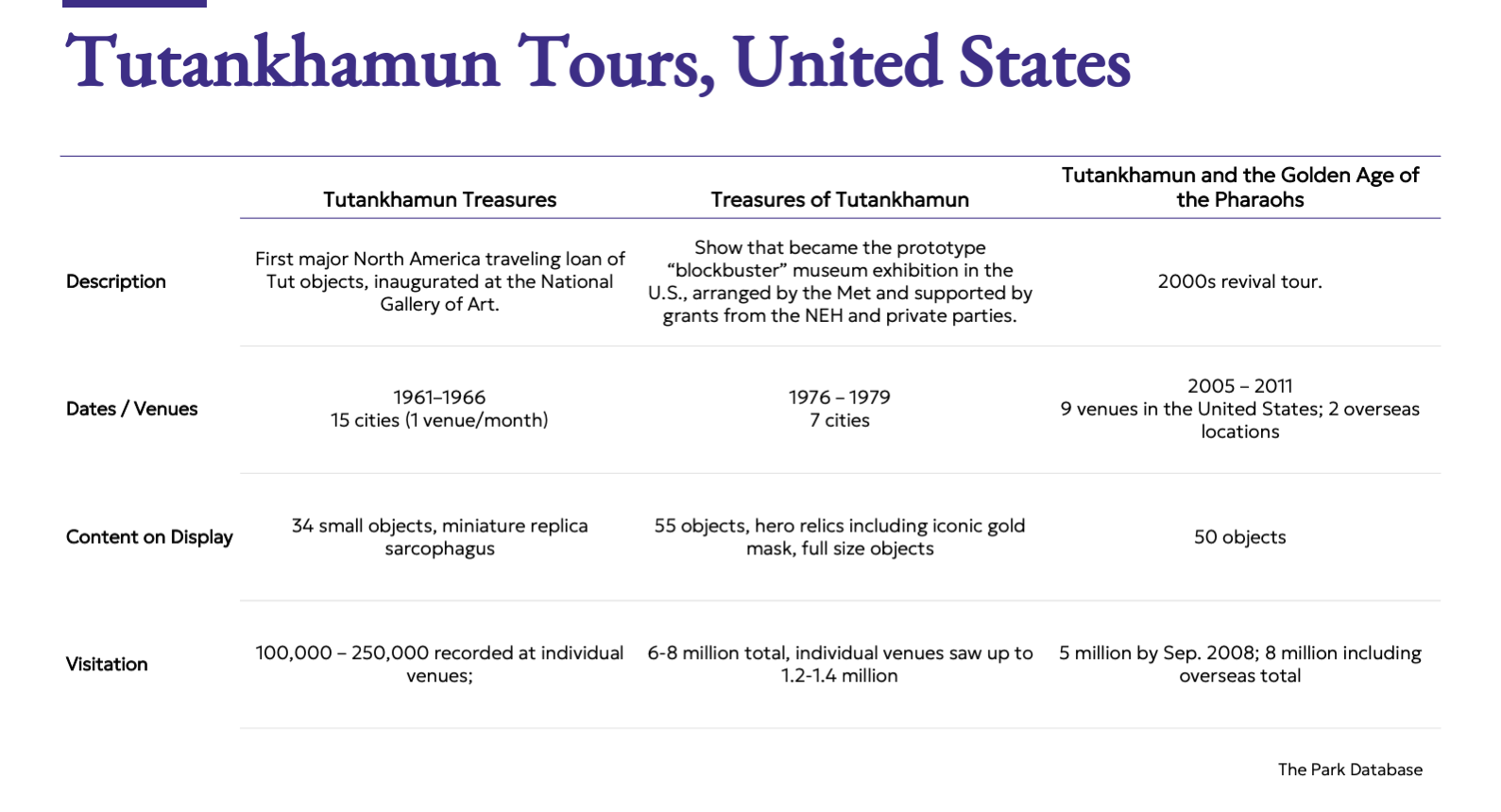

The 1960s Tour: Academic Success

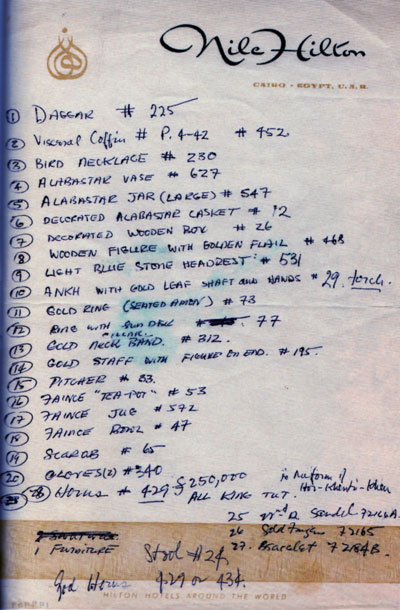

In the early 1960s, a touring exhibition of Egyptian artifacts, including 35 objects and a sarcophagus, traveled to major U.S. institutions.

The exhibition toured 14 cities over two years. Attendance at the National Gallery of Art approached 250,000 and was opened by Jacqueline Kennedy. At the Chicago Museum of Natural History in 1962, 123,722 visitors attended, “ranking the showing among the Museum’s most popular presentations”.

At the time, it was heralded as a major success. The Field Museum annual report noted that attendance was supported by “the most comprehensive publicity campaign yet undertaken by the Division of Public Relations,” included mailing lists, circulars, newspapers, radio, and newsreels.

The 1970s Tour: A Cultural Event

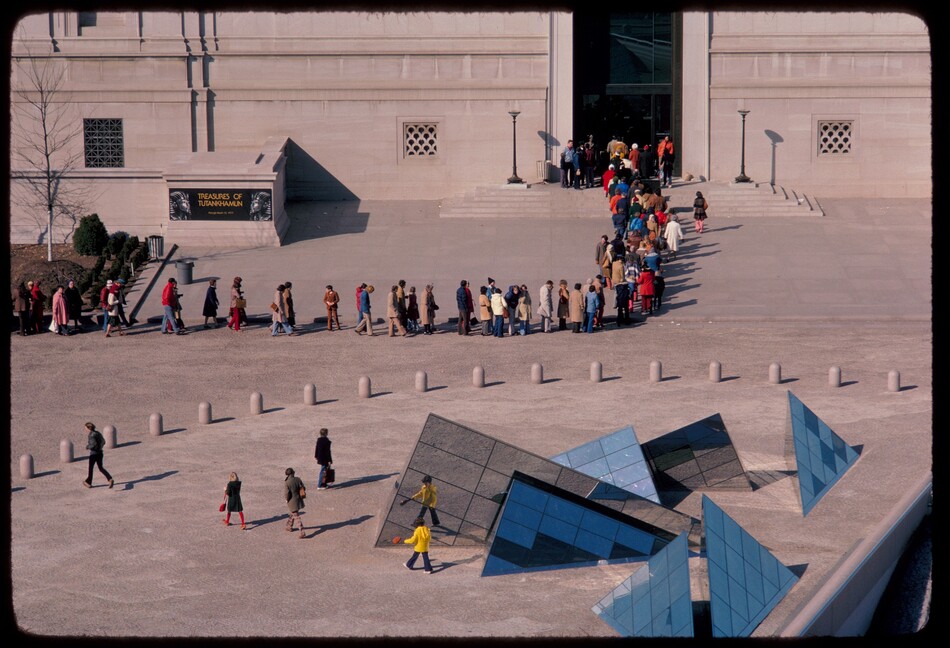

A decade later, a similar exhibition returned to the United States; this time organized by the Metropolitan Museum of Art, and touring six cities over two years.

The difference was dramatic. Over 8 million total tickets were sold. Tickets at the Met sold out in six days. On the day of some venue openings, crowds lined up at 2 a.m., eight hours before opening. The 1.2 million visitors who attended the Los Angeles County Museum of Art (LACMA) showing made it the highest attended exhibition in its history; the Met’s 1979 exhibition held the museum’s most-visited record until 2018.

Visitation per venue was often nearly an order of magnitude higher than in the 1960s tour. At Chicago’s Field Museum, the 1962 exhibit was visited by a record 123,722; its 1977 exhibit recorded 1,348,000 visitors.

What changed? With a lack of primary sources for the first exhibition, we can only rely on educated guesses.

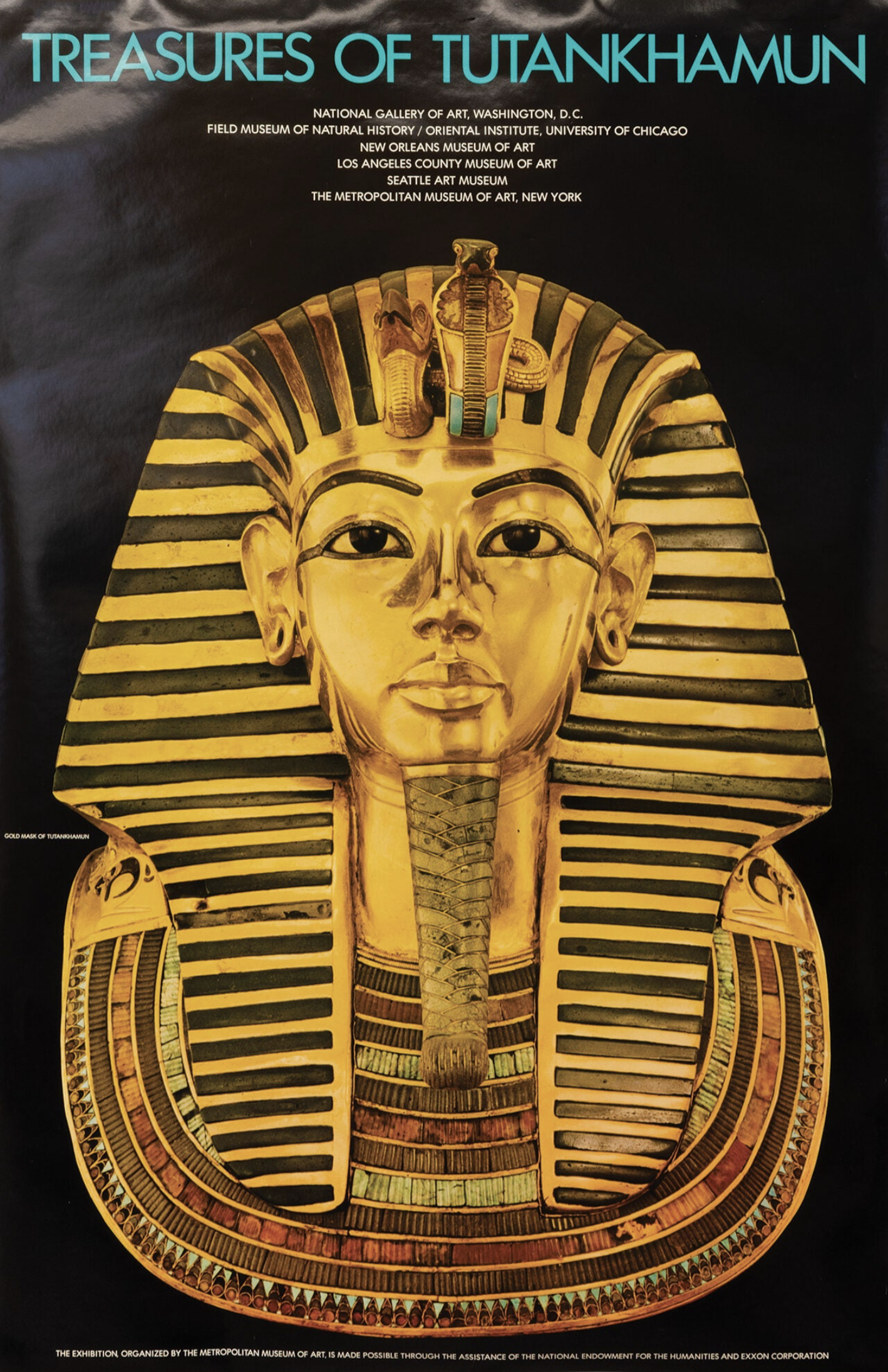

For starters, the later exhibit was bigger in terms of content. Whereas the first exhibition displayed only ’35 small-scale objects’, the second exhibition included 55 pieces, including landmark pieces, with abundant references to ‘gold’.

The second tour was also longer in terms of run times, spending four months at each stop whereas the first had allocated only a month per stop – albeit across more than double the number of venues.

The 1970s tour was also heavily promoted and supported by US grants, which covered the cost of its production. And undoubtedly experience on the part of the Egyptian government played a part as well – by the late 1970s, the artifacts had gone through a British tour, with associated learnings.

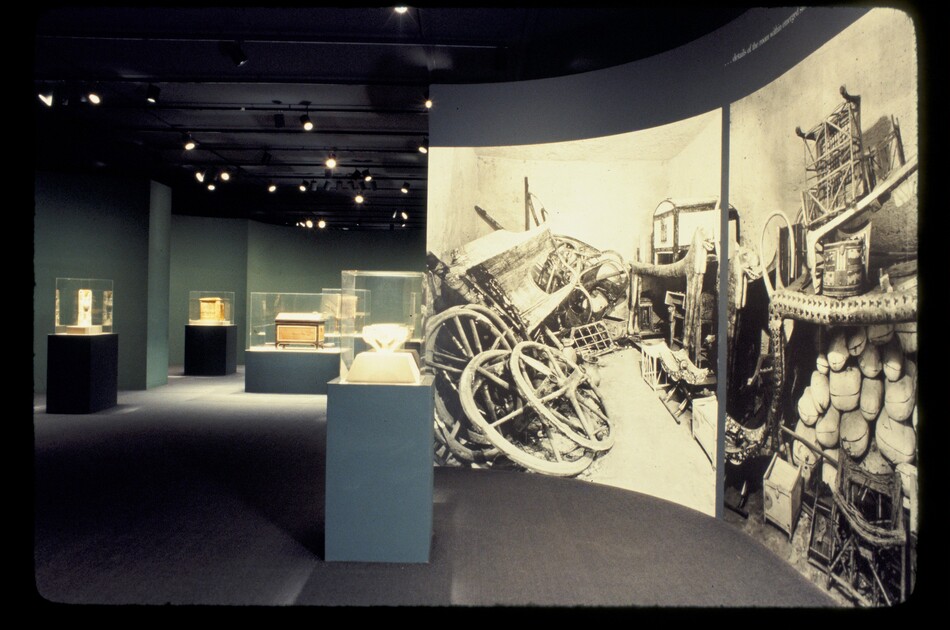

But there was also a subtle shift – whereas the earlier run was more academic and educational in nature, the second tour was marketed as a true attraction and event. It foregrounded the “boy king,” placing Tutankhamun’s gold funerary mask front and center in promotional posters. It emphasized gold. It designed the exhibit like an immersive expeirence, recreating Howard Carter’s discovery, incorporating immersive staging elements.

In striking contrast to the earlier exhibition, this tour generated a massive amount of iconography in the form of posters, imagery, and mass-market branding that permanently embedded itself in popular culture and the national consciousness.

The exhibition returned to the United States for a third and fourth time, in the 2000s, but visitation did not break any new records. At LACMA, visitation during the 2005 tour was 25% lower than during the 1978 stop. It seems the step change in marketing had already been spent.

In recent years, King Tut has met a similar fate as the art masters, with dilution in the form of numerous competing tours and exhibits.

Traveling exhibitions sit at the intersection of museum curation, theatrical production, and speculative real estate. They reset every time they move. Their presence, popularity, and profits can be ephemeral. But when the narrative and market conditions align just right, they can create history.

For data on this product type, be sure to check out our exhibits brief.